Free Cg 20 10 07 04 Liability Endorsement Template

The CG 20 10 07 04 Liability Endorsement form plays a crucial role in the realm of commercial general liability insurance. This endorsement is designed to extend coverage to additional insured parties, such as owners, lessees, or contractors, specified in a schedule. It modifies the existing insurance policy to include these additional insureds, but only for liability arising from bodily injury, property damage, or personal and advertising injury linked to the actions or omissions of the primary insured or their representatives. Notably, the coverage is limited to ongoing operations at designated locations and is subject to specific legal constraints. If the endorsement is tied to a contractual obligation, the coverage will not exceed what is stipulated in that contract. Furthermore, the form outlines exclusions, particularly concerning injuries or damages that occur after the completion of work or when the work has been put to its intended use. Importantly, the limits of insurance for the additional insureds are capped at either the amount required by the contract or the available limits under the policy, whichever is lower. Understanding these key components is essential for anyone involved in contracts that require additional insured status, ensuring clarity and protection in liability matters.

Document Specifics

| Fact Name | Description |

|---|---|

| Policy Number | This endorsement is identified by the policy number CG 20 10 12 19. |

| Purpose | The endorsement adds additional insured status for owners, lessees, or contractors. |

| Coverage Modification | It modifies the insurance provided under the Commercial General Liability Coverage Part. |

| Additional Insured | Includes persons or organizations listed in the schedule for liability coverage. |

| Liability Scope | Covers liability for bodily injury, property damage, and personal and advertising injury. |

| Acts or Omissions | Coverage applies to acts or omissions by the named insured or those acting on their behalf. |

| Legal Limitations | Coverage is only effective to the extent permitted by law. |

| Contractual Limitations | If required by contract, coverage cannot exceed what the contract mandates. |

| Exclusions | Excludes coverage for injuries or damages after project completion or intended use. |

| Limit of Insurance | The endorsement does not increase the applicable limits of insurance. |

Similar forms

CG 20 10 12 19 – Additional Insured Endorsement: This document is similar because it also extends coverage to additional insured parties. Like the CG 20 10 07 04, it modifies the general liability policy to include specific individuals or organizations, ensuring they are protected against liabilities arising from the named insured's operations.

CG 20 37 07 04 – Additional Insured – Owners, Lessees, or Contractors (Completed Operations): This endorsement shares similarities as it provides coverage for additional insureds, but specifically focuses on completed operations. It ensures that once the work is finished, the additional insureds are still protected against claims that may arise from that work.

CG 20 33 07 04 – Additional Insured – Owners, Lessees, or Contractors (Designated Projects): This document is akin to the CG 20 10 07 04 in that it adds coverage for additional insureds but is limited to designated projects. This means that the coverage applies only to specific projects listed in the endorsement, aligning with the need for targeted protection.

Ohio Medical Power of Attorney: For those preparing for healthcare decisions, our comprehensive Ohio Medical Power of Attorney resources ensure your preferences are upheld when you cannot advocate for yourself.

CG 21 44 07 04 – Additional Insured – Managers or Lessors of Premises: This endorsement is similar as it expands coverage to managers or lessors of premises. Like the CG 20 10 07 04, it protects these parties from liabilities related to the insured's operations on the premises they manage or lease.

CG 20 10 04 13 – Additional Insured – Designated Person or Organization: This document is comparable because it also allows for the addition of specific individuals or organizations as insureds. It modifies the general liability policy to provide coverage for liabilities arising from the named insured’s operations, similar to the CG 20 10 07 04.

Cg 20 10 07 04 Liability Endorsement Example

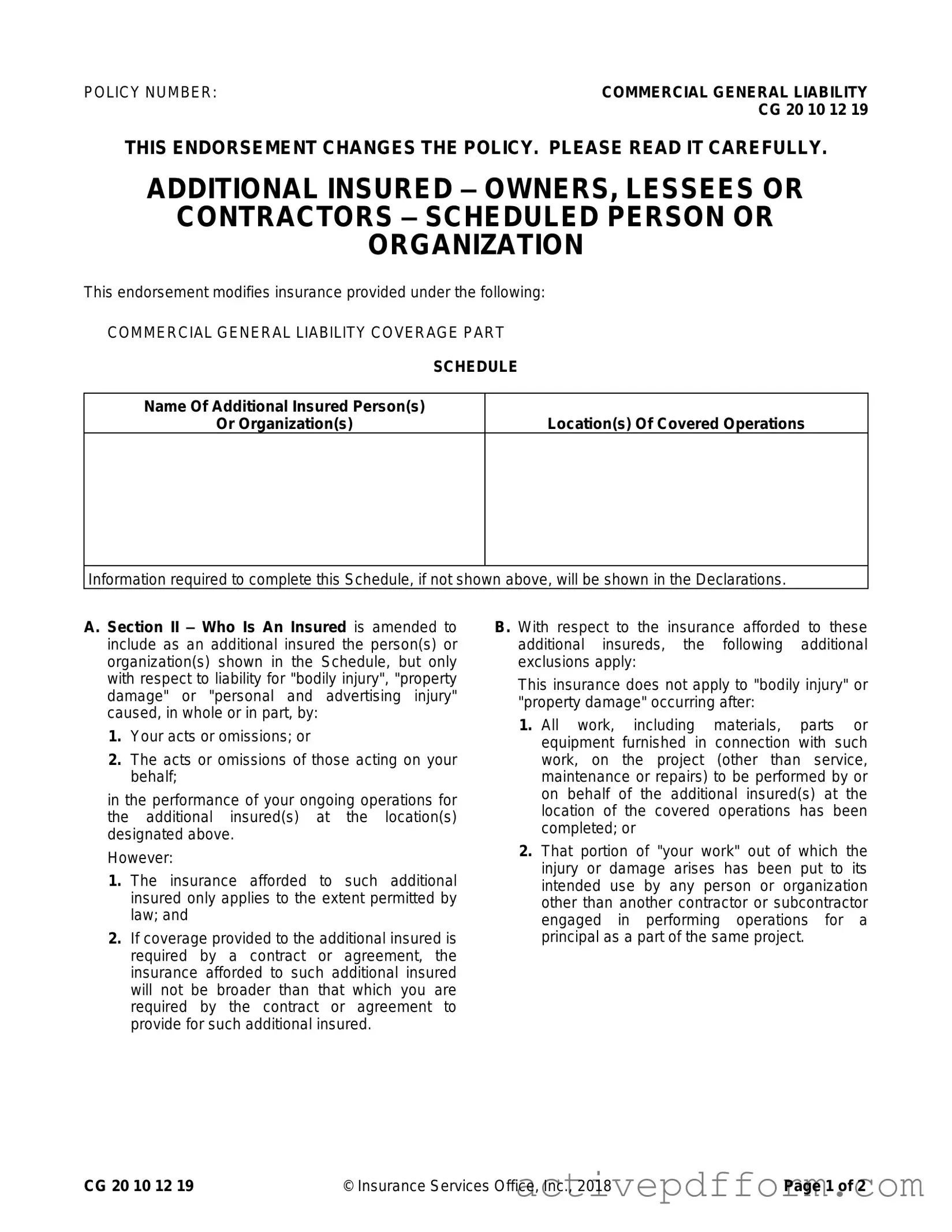

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 10 12 19 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR

CONTRACTORS – SCHEDULED PERSON OR

ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location(s) Of Covered Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by:

1.Your acts or omissions; or

2.The acts or omissions of those acting on your behalf;

in the performance of your ongoing operations for the additional insured(s) at the location(s) designated above.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following additional exclusions apply:

This insurance does not apply to "bodily injury" or "property damage" occurring after:

1.All work, including materials, parts or equipment furnished in connection with such work, on the project (other than service, maintenance or repairs) to be performed by or on behalf of the additional insured(s) at the location of the covered operations has been completed; or

2.That portion of "your work" out of which the injury or damage arises has been put to its intended use by any person or organization other than another contractor or subcontractor engaged in performing operations for a principal as a part of the same project.

CG 20 10 12 19 |

© Insurance Services Office, Inc., 2018 |

Page 1 of 2 |

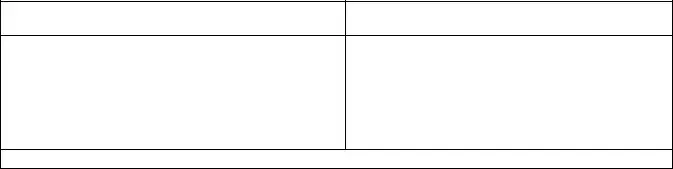

C. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable limits of insurance;

whichever is less.

This endorsement shall not increase the applicable limits of insurance.

Page 2 of 2 |

© Insurance Services Office, Inc., 2018 |

CG 20 10 12 19 |

Understanding Cg 20 10 07 04 Liability Endorsement

What is the purpose of the CG 20 10 07 04 Liability Endorsement form?

The CG 20 10 07 04 Liability Endorsement form is designed to extend coverage to additional insured parties, such as owners, lessees, or contractors. This endorsement modifies the existing Commercial General Liability policy to include specific individuals or organizations as additional insureds. The coverage applies to liabilities arising from bodily injury, property damage, or personal and advertising injury that may occur during the performance of ongoing operations at designated locations.

Who qualifies as an additional insured under this endorsement?

Individuals or organizations listed in the endorsement's schedule are considered additional insureds. The coverage applies specifically to liabilities that result from your actions or the actions of those working on your behalf while performing operations for these additional insureds. It is important to note that this coverage is limited to the locations and operations specified in the endorsement.

Are there any limitations to the coverage provided to additional insureds?

Yes, there are limitations. The coverage for additional insureds is only applicable to the extent permitted by law and cannot exceed what is required by any contract or agreement. Additionally, the endorsement specifies that coverage does not apply to bodily injury or property damage that occurs after the completion of all work on the project or when the work has been put to its intended use by someone other than another contractor or subcontractor involved in the same project.

What are the limits of insurance for additional insureds?

The limits of insurance for additional insureds are defined by the endorsement. If coverage is required by a contract, the maximum amount payable on behalf of the additional insured is the lesser of the amount required by that contract or the available limits under the policy. Importantly, this endorsement does not increase the overall limits of insurance provided by the policy.

How should I complete the schedule for additional insureds?

To complete the schedule for additional insureds, you will need to provide the names of the individuals or organizations that should be covered, along with the specific locations of the operations for which they will be insured. If this information is not included in the endorsement itself, it will typically be documented in the policy's declarations page. Ensuring that this information is accurate is crucial for the effective application of the coverage.

Dos and Don'ts

When filling out the CG 20 10 07 04 Liability Endorsement form, attention to detail is crucial. Here are six important do's and don'ts to guide you through the process:

- Do read the entire endorsement carefully to understand its implications on your coverage.

- Do ensure that the names of all additional insured persons or organizations are spelled correctly in the schedule.

- Do provide accurate locations of covered operations to avoid any potential coverage disputes.

- Don't leave any sections blank; incomplete forms can lead to delays or denial of coverage.

- Don't assume that the coverage for additional insureds is broader than what is required by your contract.

- Don't forget to review the exclusions listed in the endorsement, as they can affect your liability coverage.

By following these guidelines, you can ensure a smoother process and greater peace of mind regarding your insurance coverage.

Check out Common Templates

Dekalb County Water New Service Application - Applicants are encouraged to provide feedback on the water service application process.

For those navigating the complexities of securing housing, the NYC Housing Application Form serves as an essential tool. This document not only streamlines the application process but also provides vital information about eligibility, covering aspects such as income and family structure. To further assist applicants, resources can be found at https://nytemplates.com/blank-nyc-housing-application-template/, ensuring they are well-prepared to take the necessary steps toward obtaining affordable housing in New York City.

How to Update Dd214 - This form is necessary for alterations related to health records in military service.